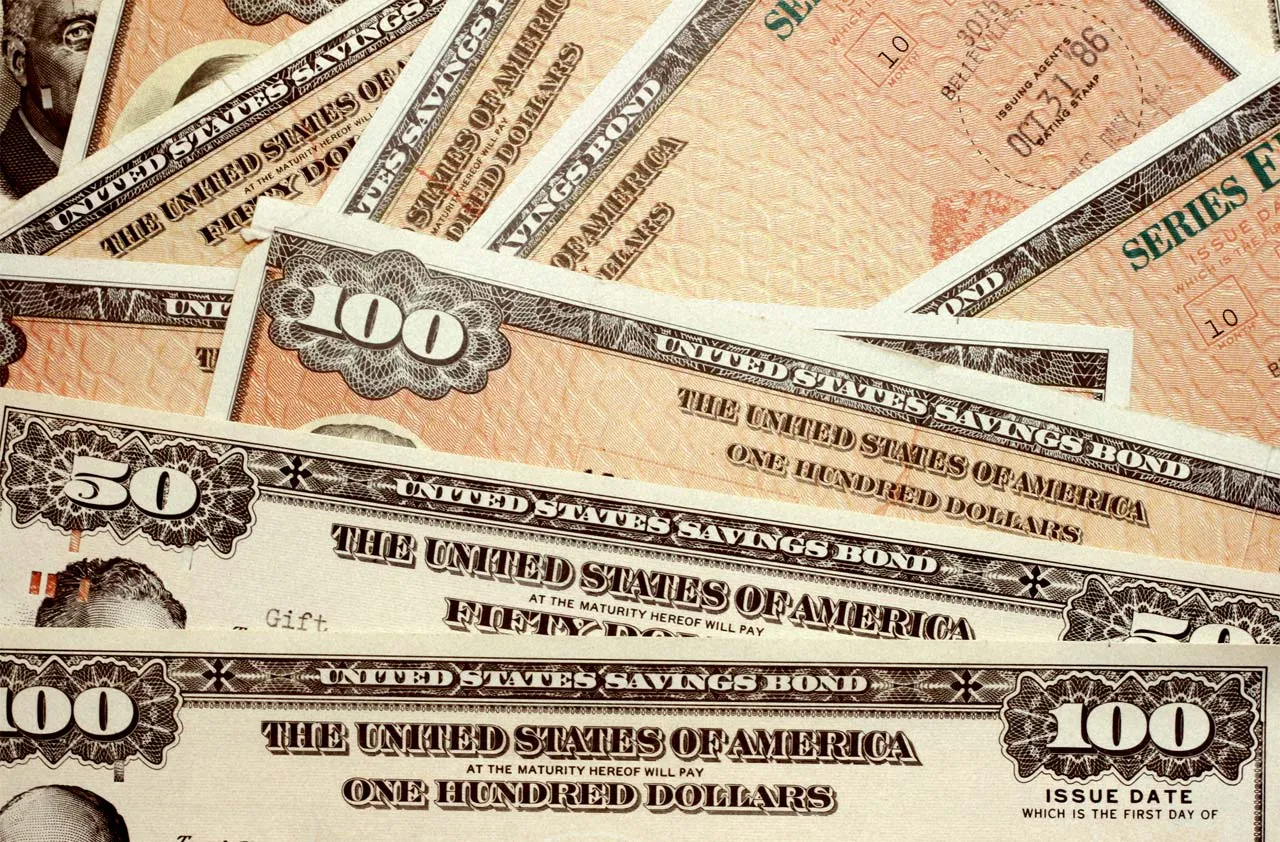

What to Do With Old Savings Bonds

First, check to see whether they are still earning interest. If not, cash them in and invest the money somewhere else.

You are now subscribed

Your newsletter sign-up was successful

Want to add more newsletters?

Delivered daily

Kiplinger Today

Profit and prosper with the best of Kiplinger's advice on investing, taxes, retirement, personal finance and much more delivered daily. Smart money moves start here.

Sent five days a week

Kiplinger A Step Ahead

Get practical help to make better financial decisions in your everyday life, from spending to savings on top deals.

Delivered daily

Kiplinger Closing Bell

Get today's biggest financial and investing headlines delivered to your inbox every day the U.S. stock market is open.

Sent twice a week

Kiplinger Adviser Intel

Financial pros across the country share best practices and fresh tactics to preserve and grow your wealth.

Delivered weekly

Kiplinger Tax Tips

Trim your federal and state tax bills with practical tax-planning and tax-cutting strategies.

Sent twice a week

Kiplinger Retirement Tips

Your twice-a-week guide to planning and enjoying a financially secure and richly rewarding retirement

Sent bimonthly.

Kiplinger Adviser Angle

Insights for advisers, wealth managers and other financial professionals.

Sent twice a week

Kiplinger Investing Weekly

Your twice-a-week roundup of promising stocks, funds, companies and industries you should consider, ones you should avoid, and why.

Sent weekly for six weeks

Kiplinger Invest for Retirement

Your step-by-step six-part series on how to invest for retirement, from devising a successful strategy to exactly which investments to choose.

Question: My parents and grandparents gave me some savings bonds when I was born. How can I figure out if they’re still earning interest? If they aren’t earning interest anymore, how do I cash them in?

Answer: The maturity date depends on the type of savings bond and when it was issued. Most savings bonds earn interest for 30 years, although HH bonds earn interest for 20 years, and old Series E bonds (from November 1965 and earlier) earn interest for 40 years. If you have E bonds or H bonds, they aren’t earning interest anymore; neither are EE bonds issued from January 1980 through April 1987 or HH bonds issued from January 1980 through April 1997. See the full list by date at TreasuryDirect.

If you have Series E bonds issued in 1974 or later or Series EE bonds, you can use the Treasury Hunt tool to quickly see if any bonds registered with your Social Security number have stopped earning interest.

From just $107.88 $24.99 for Kiplinger Personal Finance

Become a smarter, better informed investor. Subscribe from just $107.88 $24.99, plus get up to 4 Special Issues

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more - straight to your e-mail.

Profit and prosper with the best of expert advice - straight to your e-mail.

If you discover that your savings bonds have matured, you should cash them in and invest the money elsewhere. If you have paper bonds, contact your bank to see if it cashes savings bonds (not all banks do, and some will cash in savings bonds only for customers who have had accounts for at least six months). For more information, see How to Cash in Savings Bonds.

If you have Series E, EE or I bonds, another option is to use the Smart Exchange at TreasuryDirect to convert your paper savings bonds to electronic bonds, which will make them much easier to monitor and redeem (you can link your TreasuryDirect account to a bank account). For more information, see Converting Paper Savings Bonds to Electronic Form.

If you can’t locate a paper bond, you can fill out Form 1048, Claim for Lost, Stolen or Destroyed U.S. Savings Bonds, and the Treasury will search its records. Provide your name and Social Security number (and the purchaser’s Social Security number, if the bond was received as a gift), the approximate issue date (or at least a range of years), the serial number, if available, and any other information you may have, such as the bond series or denomination. If you don’t have all of this information, fill out as much as you can. Get the form certified by a financial institution, and send it to the address listed on the form for the type of bond you’re trying to track down. For more information, see Tracking Down Missing Savings Bonds.

-

Dow Leads in Mixed Session on Amgen Earnings: Stock Market Today

Dow Leads in Mixed Session on Amgen Earnings: Stock Market TodayThe rest of Wall Street struggled as Advanced Micro Devices earnings caused a chip-stock sell-off.

-

How to Watch the 2026 Winter Olympics Without Overpaying

How to Watch the 2026 Winter Olympics Without OverpayingHere’s how to stream the 2026 Winter Olympics live, including low-cost viewing options, Peacock access and ways to catch your favorite athletes and events from anywhere.

-

Here’s How to Stream the Super Bowl for Less

Here’s How to Stream the Super Bowl for LessWe'll show you the least expensive ways to stream football's biggest event.

-

How Are I Bonds Taxed? 8 Common Situations to Know

How Are I Bonds Taxed? 8 Common Situations to KnowBonds Series I U.S. savings bonds are a popular investment, but the federal income tax consequences are anything but straightforward.

-

How Are I Bonds Taxed? Nine Common Situations

How Are I Bonds Taxed? Nine Common SituationsBonds Series I bonds are a popular investment that can help you save on taxes, but the federal income tax consequences can be complex.

-

Bond Basics: U.S. Savings Bonds

Bond Basics: U.S. Savings Bondsinvesting U.S. savings bonds are a tax-advantaged way to save for higher education.

-

Short-Term Investments to Protect Against Inflation and Market Volatility

Short-Term Investments to Protect Against Inflation and Market VolatilityRates on Series I savings bonds, T-bills and fixed annuities are all above historical averages and could serve investors well during turbulent times like these.

-

What Are I-Bonds? Inflation Made Them Popular. What Now?

What Are I-Bonds? Inflation Made Them Popular. What Now?savings bonds Inflation has made Series I savings bonds, known as I-bonds, enormously popular with risk-averse investors. How do they work?

-

PODCAST: Changes Coming to Flood Insurance with Laura Lightbody

PODCAST: Changes Coming to Flood Insurance with Laura LightbodyBecoming a Homeowner The National Flood Insurance Program is getting an overhaul that could send your rates up (or down). We dig into what's changing with this coverage that many have—and many more need. Also, a bond that pays over 7 percent, for now.

-

What Grandparents Need to Know About Using Savings Bonds for a Grandchild’s Education

What Grandparents Need to Know About Using Savings Bonds for a Grandchild’s EducationTax Breaks It’s not easy, but grandparents can avoid a tax bill when redeeming savings bonds to pay for a grandchild’s college costs.

-

How to Add Treasury Bonds, Bills and Notes to an IRA

How to Add Treasury Bonds, Bills and Notes to an IRAinvesting If you are wondering how to add Treasury bills, bonds and notes to an IRA, there are ways to do so.