Cell Phone Screw-up Solved

Cell-phone taxes are based on the area you told the provider would be your primary place of use.

You are now subscribed

Your newsletter sign-up was successful

Want to add more newsletters?

Delivered daily

Kiplinger Today

Profit and prosper with the best of Kiplinger's advice on investing, taxes, retirement, personal finance and much more delivered daily. Smart money moves start here.

Sent five days a week

Kiplinger A Step Ahead

Get practical help to make better financial decisions in your everyday life, from spending to savings on top deals.

Delivered daily

Kiplinger Closing Bell

Get today's biggest financial and investing headlines delivered to your inbox every day the U.S. stock market is open.

Sent twice a week

Kiplinger Adviser Intel

Financial pros across the country share best practices and fresh tactics to preserve and grow your wealth.

Delivered weekly

Kiplinger Tax Tips

Trim your federal and state tax bills with practical tax-planning and tax-cutting strategies.

Sent twice a week

Kiplinger Retirement Tips

Your twice-a-week guide to planning and enjoying a financially secure and richly rewarding retirement

Sent bimonthly.

Kiplinger Adviser Angle

Insights for advisers, wealth managers and other financial professionals.

Sent twice a week

Kiplinger Investing Weekly

Your twice-a-week roundup of promising stocks, funds, companies and industries you should consider, ones you should avoid, and why.

Sent weekly for six weeks

Kiplinger Invest for Retirement

Your step-by-step six-part series on how to invest for retirement, from devising a successful strategy to exactly which investments to choose.

Although I live in Rhode Island, this month the taxes, surcharges and fees on my Sprint wireless bill increased due to myriad new charges from Vancouver, Wash.; Clark County, where Vancouver is located; and Washington State. SprintÕs customer-service representative explained that I would have to pay the taxes because my coverage area had changed. Another rep said that I could be charged state taxes just by staying in a state for a week (although I havenÕt been to the West Coast in more than a year). Is this a common billing practice among wireless companies? -- George Kelley, Greenville, R.I.

No way. It's not even a common practice at Sprint, which admits that the taxes on your bill were a mistake and that you were misinformed by its representatives.

Cell-phone taxes, surcharges and fees, which often add up to more than 15% of your monthly bill, are based on the area you tell the service provider will be your primary place of use. That means you can be taxed by your home state, county, city or local district, but your taxes shouldn't be affected by changes in your service area or by travel. Nor should you be taxed by another jurisdiction just because you've made calls within its borders.

From just $107.88 $24.99 for Kiplinger Personal Finance

Become a smarter, better informed investor. Subscribe from just $107.88 $24.99, plus get up to 4 Special Issues

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more - straight to your e-mail.

Profit and prosper with the best of expert advice - straight to your e-mail.

We asked Sprint to investigate, and the company discovered that until you retired in July 2006, your phone service was billed as a business account. When you asked to switch to a personal account but keep your phone number, Sprint's service rep should have asked for your primary place of use, which is Greenville, R.I. And you should have been charged federal, state and local taxes only for that area. Instead, you were erroneously charged taxes based on the move by your former employer's accounting office to Washington State.

P.S. To atone for its mistake, Sprint gave Kelley free phone service for a month.

Escape a "value trap"

You've warned about cheap stocks you labeled "value traps." What are value traps, and how do investors avoid them? -- Cordell Larkin, Chicago

Easier said than done. Value traps -- cheap stocks that turn out to be stinkers -- are like mirages: You think you've found a bargain-priced oasis only to end up eating sand. "It's a real pitfall for value managers," says Peter Morris, manager of Homestead Value fund, which invests in beaten-down companies. "There's no formula to help you steer clear of value traps."

Often stocks that trade at low price-earnings ratios or similar measures of value are cheap for good reason.Investors need to figure out whether the malaise affecting a company is a temporary setback or the start of a death spiral.

In the late 1990s, Morris thought shares of Oneida, a maker of china and flatware, were a steal because of the company's low stock price and popular brand name. But global competition and a bloated infrastructure wrecked Oneida's finances, and the company filed for bankruptcy in 2006. Warning signs of a value trap "don't appear all at once," says Morris. "It's a slow, deteriorating process."

Stick with companies that have a sustainable product or service, Morris advises -- ideally, those whose true value has been misjudged by investors. And you want to avoid companies in moribund industries or those with declining market share. Also, a business with little or no debt that generates plenty of cash is less likely to be a value trap than one with a weak balance sheet.

Home-sale profits

My husband just took a new job about 75 miles away. We want to sell the house we bought in July 2006 and hope to make a profit of about $100,000. Will we have to pay capital-gains tax? -- J.C., Joplin, Mo.

Good luck making a $100,000 profit after only a year given today's housing market. As for your tax question, you generally need to own and live in your home for two of the five years preceding the sale in order to qualify for a capital-gains tax break. But thanks to your husband's new job, you may still be able to shelter part of your home-sale profit from taxes.

Married couples filing jointly who meet the residency rule don't owe capital-gains tax on a home-sale profit of up to $500,000 (or $250,000 for single filers). So, for example, a married couple who bought a house for $300,000 wouldn't have to pay taxes unless they sold the house for more than $800,000. People who don't meet the two-out-of-five-year rule generally must pay taxes on their profit -- either at the 15%, long-term capital-gains rate (if they've owned the home for longer than a year) or at their income-tax rate (if they've owned it for one year or less).

[page break]

But there are a few exceptions, and your husband's job switch qualifies as one of them. If the new job is at least 50 miles farther from your old home than the previous job was, you can prorate your tax exclusion based on the number of months you owned and lived in the house.

Suppose you sell your home after 14 months. In that case, 58.3% of the profit (14 out of 24 months) qualifies for the exclusion. So, for a married couple, a total of $291,500 in profits could escape capital-gains taxes.

Home sellers can also qualify for a partial exclusion if they move in less than two years because of their health or the health of family members in their care, or if they're affected by other unforeseen circumstances approved by the IRS, such as death, divorce, unemployment or damage to the home as the result of a disaster (for more details, see IRS Publication 523, Selling Your Home).

College tax breaks

If we set up a 529 college-savings account for our children, can grandparents, other family members and friends get a tax benefit when they contribute? -- Stephanie Curtis, via e-mail

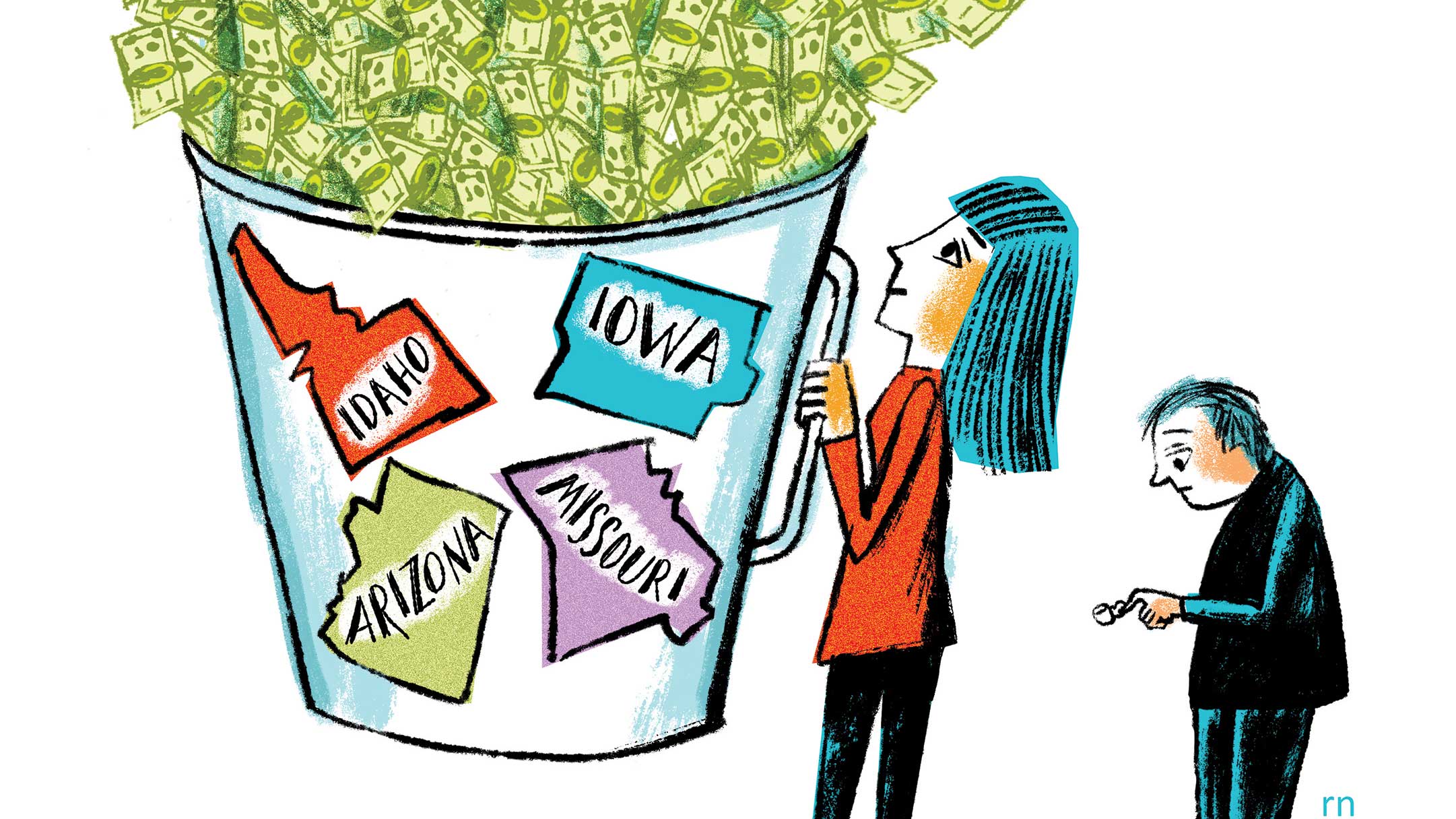

It depends on the state. Assuming your state offers a tax deduction for contributions to a 529 plan, you generally must invest in your own state's plan to qualify. Residents of Kansas, Maine and Pennsylvania can get a tax break no matter where they invest.

But states differ on who's entitled to the deduction. In some states, such as Iowa and Missouri, you have to own the account in order to claim the deduction. Wisconsin allows even nonowners to take a deduction of up to $3,000 per beneficiary per return -- but only if you contribute on behalf of dependents, grandchildren, great-grandchildren, nieces or nephews (or for the account owner's own benefit).

Virginia lets an account owner claim a deduction for contributions made by other people -- but doesn't let nonowners take the deduction themselves. So it pays for generous family members and friends to open their own accounts. In any state, there's no limit on the number of accounts that may be opened for a child. And donors can open an account for the same child in any number of states to take advantage of local tax breaks (read more about state 529 plans in The Best Way to Save for College).

Best overseas card

I'm moving to Turkey for a year. I'd like to cancel my American Express card, with a high annual fee, and get a no-fee card that offers rewards (mainly airline miles) and can be used abroad without charges. -- Marlene Atzal, Annandale, Va.

The no-fee Capital One No Hassle Miles Rewards card is a good alternative. Capital One doesn't charge a currency-conversion fee on overseas purchases, nor does it pass on the 1% fee that MasterCard and Visa charge.

You earn 1.25 miles for each dollar you spend, but it might take a while to accumulate enough miles for a free trip. Capital One bases the number of miles needed on the price of the ticket. You must accrue 35,000 miles to exchange them for a ticket that costs $150 to $350. Miles don't expire, and there's no limit on the mileage you can earn.

My thanks to Joan Goldwasser and Tom Anderson for their help this month.

-

How Much It Costs to Host a Super Bowl Party in 2026

How Much It Costs to Host a Super Bowl Party in 2026Hosting a Super Bowl party in 2026 could cost you. Here's a breakdown of food, drink and entertainment costs — plus ways to save.

-

3 Reasons to Use a 5-Year CD As You Approach Retirement

3 Reasons to Use a 5-Year CD As You Approach RetirementA five-year CD can help you reach other milestones as you approach retirement.

-

Your Adult Kids Are Doing Fine. Is It Time To Spend Some of Their Inheritance?

Your Adult Kids Are Doing Fine. Is It Time To Spend Some of Their Inheritance?If your kids are successful, do they need an inheritance? Ask yourself these four questions before passing down another dollar.

-

Kiplinger's Tax Map for Middle-Class Families: About Our Methodology

Kiplinger's Tax Map for Middle-Class Families: About Our Methodologystate tax The research behind our judgments.

-

Retirees, Make These Midyear Moves to Cut Next Year's Tax Bill

Retirees, Make These Midyear Moves to Cut Next Year's Tax BillTax Breaks Save money next April by making these six hot-as-July tax moves.

-

Estimated Payments or Withholding in Retirement? Here's Some Guidance

Estimated Payments or Withholding in Retirement? Here's Some GuidanceBudgeting You generally must pay taxes throughout the year on your retirement income. But it isn't always clear whether withholding or estimated tax payments is the best way to pay.

-

How to Cut Your 2021 Tax Bill

How to Cut Your 2021 Tax BillTax Breaks Our guidance could help you claim a higher refund or reduce the amount you owe.

-

Why This Tax Filing Season Could Be Ugly

Why This Tax Filing Season Could Be UglyCoronavirus and Your Money National Taxpayer Advocate Erin M. Collins warns the agency will continue to struggle with tight budgets and backlogs. Her advice: File electronically!

-

Con Artists Target People Who Owe The IRS Money

Con Artists Target People Who Owe The IRS MoneyScams In one scheme, thieves will offer to "help" you pay back taxes, only to leave you on the hook for expensive fees in addition to the taxes.

-

Cash-Rich States Lower Taxes

Cash-Rich States Lower TaxesTax Breaks The economic turnaround sparked a wave of cuts in state tax rates. But some say the efforts could backfire.

-

The Financial Effects of Losing a Spouse

The Financial Effects of Losing a SpouseFinancial Planning Even amid grief, it's important to reassess your finances. With the loss of your spouse's income, you may find yourself in a lower tax bracket or that you qualify for new deductions or credits.